The MAGA Tax

The hidden “MAGA tax” may be costing America nearly a full point of economic growth

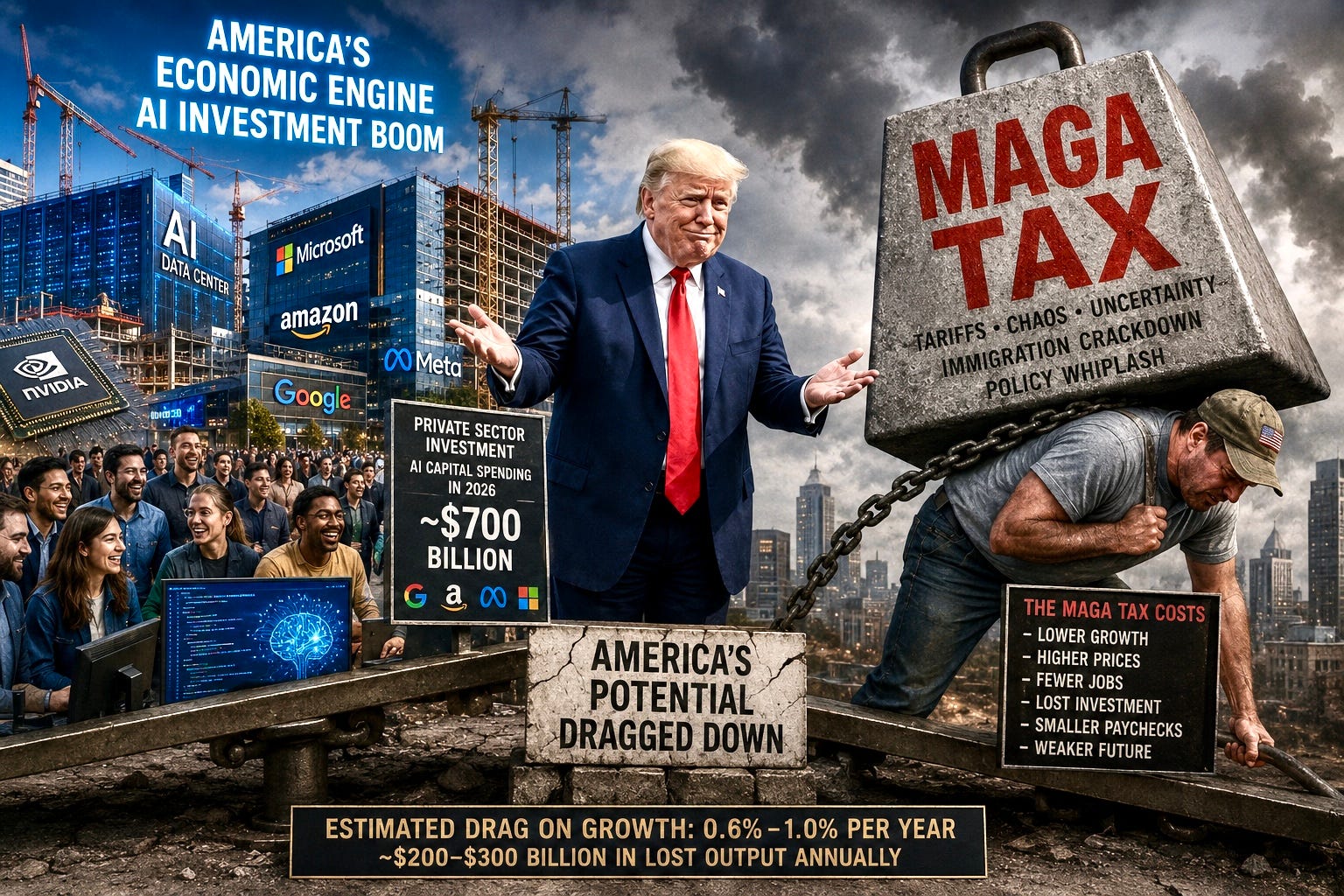

The American economy is executing an extraordinary balancing act unprecedented in modern history. On one side, a formidable private-sector engine drives growth—marked by an artificial-intelligence investment surge, record corporate spending on data centers and chips, resilient consumer demand, rising equity markets, and an innovation cycle poised to reshape entire industries simultaneously. On the other side stands Donald Trump.

The economic story of 2026 clearly isn’t that Trump destroyed the economy. He didn’t. The economy is too large, too dynamic, and too structurally innovative for that. The true story is more subtle—and potentially more significant.

Trump is effectively imposing a hidden national tax on America's economic potential—a drag tax, a friction tax, a chaos tax—a MAGA tax.

The evidence suggests the US economy is growing significantly slower than it otherwise would because of the administration’s trade wars, immigration crackdowns, policy volatility, and constant climate of uncertainty. The extraordinary part is that the economy still looks relatively strong anyway, largely because AI investment and financial-market momentum are masking the damage underneath.

That distinction matters enormously. If the economy is growing at 2.1% while dragging around nearly a full percentage point of avoidable, self-inflicted political damage, then the real story isn’t resilience alone—it’s squandered capacity on a historic scale. In plain English: America’s economy may currently be succeeding despite Trump, not because of him.

The administration inherited a remarkably durable economic machine. Productivity growth had improved, corporate balance sheets were healthy, unemployment remained low, and technological investment was accelerating. Then came the AI explosion.

Alphabet, Amazon, Meta, and Microsoft alone are projected to spend roughly $700 billion on AI-related capital expenditures in 2026. That isn’t normal business expansion—it’s industrial-scale economic mobilization. Data centers, semiconductors, cooling systems, energy infrastructure, fiber networks, cloud systems, and software investment are all exploding simultaneously. The AI boom is now so large that it’s acting almost like a parallel stimulus program run by the private sector itself.

Meanwhile, the stock market surged after Trump’s election victory, adding trillions in household wealth that consumers spent down in pieces. Tax cuts and deregulation provided additional stimulus. By themselves, those forces should have produced a genuine economic roar. Instead, what America got was something oddly muted—strong growth, yes, but nowhere near as strong as the underlying conditions suggest it should be.

That gap—the difference between what the economy is doing and what it could be doing—is where the idea of the MAGA tax becomes economically serious rather than politically rhetorical.

The measurable costs begin with tariffs. Trump’s tariffs function as taxes whether politicians admit it or not. They raise costs on imported goods, intermediate components, machinery, and industrial inputs. Businesses absorb some of the cost through lower margins, and consumers absorb the rest through higher prices. Economists across ideological lines broadly agree on this basic mechanism—it isn’t really controversial economics. Tariffs distort pricing and reduce efficiency. Full stop.

The Peterson Institute estimated Trump’s tariff escalation reduced growth in 2025 by roughly 0.2 percentage points, and other models project larger effects moving forward. The Tax Foundation estimates that tariffs amount to hundreds of billions of dollars in new taxes over time, with meaningful costs passed directly to households.

And tariffs don’t simply hit imported consumer products sitting on retail shelves. They hit supply chains, manufacturing inputs, transportation equipment, industrial planning, and capital investment decisions across every sector that touches a global market. When tariffs constantly shift—announced, paused, revised, threatened, expanded, retracted—companies stop making long-term commitments because nobody knows what the rules will be six months later.

That uncertainty may be the single biggest economic cost of the entire administration. Businesses can adapt to almost any stable environment, including high taxes, high labor costs, or complex regulations. What businesses can’t adapt to is unpredictability. Capital hates uncertainty because investment decisions are long-duration bets. A company building a factory doesn’t care only about next quarter—it cares about the next decade. And right now many executives appear increasingly unwilling to place those bets.

Strip away AI-related investment and the broader picture becomes surprisingly weak. Non-AI industrial investment has softened dramatically, manufacturing construction has fallen sharply, and equipment investment has weakened across the board. Capital expenditures outside the technology boom look far more like recessionary behavior than like economic boom behavior. That matters because broad-based investment is how economies expand future productive capacity. It’s how wages rise sustainably, how productivity improves, how nations become richer over time.

The administration’s immigration policies are producing another drag effect that receives far less attention than tariffs but may ultimately prove just as economically significant. America’s economy has long depended on labor-force expansion through immigration—labor that fuels construction, agriculture, logistics, hospitality, healthcare support, manufacturing, and increasingly even higher-skilled sectors.

Now, net migration appears to have collapsed toward zero, or possibly even into negative territory, for the first time in generations. This isn’t a cultural or political issue. It’s a macroeconomic issue. When labor-force growth slows, economic growth slows. When population growth slows, demand growth slows. When workers disappear, entire sectors face shortages, slower output, constrained expansion, and upward pressure on prices. Ironically, many of the same industries that strongly supported Trump politically are among the most dependent on immigrant labor economically. That contradiction is becoming harder to ignore.

Then there’s the broader psychological cost of governing through permanent disruption. Markets can tolerate ideological extremism, partisan conflict, and deficits. What markets truly struggle with is randomness—trade wars launched through social-media posts, constant executive threats, abrupt regulatory reversals, political attacks on the Federal Reserve, legal uncertainty surrounding entire industries, and geopolitical brinkmanship layered on top of economic brinkmanship.

An economy doesn’t collapse overnight from those conditions. Confidence slowly erodes around the edges. Companies delay hiring, projects stall, expansion plans shrink, and risk premiums rise quietly in the background. The damage accumulates gradually before it becomes visible all at once.

And yet despite all of this, the American economy keeps moving. That may be the most astonishing part of the story. The US still possesses extraordinary structural strengths: massive capital markets, technological dominance, deep consumer spending power, world-leading research ecosystems, energy abundance, and the magnetic global pull of American innovation. AI alone may ultimately become one of the largest investment booms since the internet revolution. That strength is currently masking significant policy dysfunction.

But masking isn’t the same thing as eliminating.

The best estimate emerging from multiple analyses is that Trump-era policy may be reducing growth by roughly 0.6 to 1 percentage point annually, with about 0.8 percentage points sitting near the middle of the plausible range. That may sound small. It isn’t. In a $30 trillion economy, a single percentage point represents hundreds of billions of dollars in lost output, wages, business investment, productivity, tax revenue, and opportunity. And the long-term effects compound.

This is the crucial distinction many political narratives miss: the danger isn’t necessarily immediate collapse. The danger is cumulative underperformance. Countries rarely decline because they suddenly stop functioning altogether. They decline because they gradually begin operating below their potential, while convincing themselves that everything is fine because collapse never visibly arrives.

That’s the deeper risk embedded inside the MAGA tax. America’s economy remains strong enough to withstand poor policymaking. The question is how much richer, stronger, more productive, and more stable it could already be if it weren’t constantly forced to absorb the costs of political chaos masquerading as economic strategy.